With information about High Frequency Trading doing the rounds, there was quite an interest among the student community. Prof Ramabhadran S Thirumalai had recently expounded on HFT in a recent forum. He agreed to throw more light on the subject, and given below is his analysis of different aspects of HFT. This article is based on a talk given by him at the National Surveillance Forum, held at the BSE Ltd. on June 20, 2016.

With the rise of high frequency trading (HFT) in the last few years, regulators world over are debating if HFT is good for market liquidity and stability. In a recent review of various academic findings on the impact of HFT, Menkveld (2016) notes that, though there are exceptions, HFTs have largely reduced transaction costs for all investors. But major concerns about HFTs continue to persist, most importantly i) given their speed advantage, do HFTs manipulate markets to their advantage? ii) Do they increase systemic risk? In this article, I will focus on the first only.

Some typical ways in which HFTs may manipulate markets are as follows:

1. Stuffing and Phantom Orders

2. Smoking

3. Spoofing

Stuffing is the clogging up of trading systems by HFTs, who submit and cancel multiple orders within a second. This leads to orders piling up in the buffer and slowing down the trading system. Stuffing leads to phantom orders, which are orders that are valid for less time than it takes for information about these orders to reach “normal” traders.

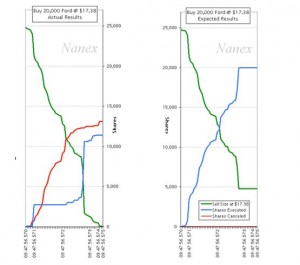

Let us look at a very simple example. A trader wants to buy 20,000 shares of Ford. The best ask price is at $ 17.38 for 24,800 shares. The buyer expects his entire buy request to trade at $ 17.38 as the shares available for sale at the best ask (24,800 shares) is greater than the 20,000 shares he wants to buy. Figure 2 shows how the trader expects his order to get executed. The blue curve keeps track of how his order filled. The green curve shows how the number of shares available for sale at $ 17.38 changes as the trader’s buy order is executed and some orders got canceled. The blue line is flat towards the right end of the graph as he purchased the entire 20,000 shares he wanted before the end of the 5 millisecond window.

However, he is able to buy only 12,133 shares and this is captured in Figure 1. The red curve shows the number of shares canceled. The red curve climbs at a faster rate than the blue curve, which tells us that when the buy order reaches the market and starts trading against sell orders at $ 17.38, traders (presumably, HFTs) start canceling their sell orders at a much faster rate. Here you can see that the blue curve flattens at a level that is slightly above 10,000 shares. The trader is unable to get his entire order of buying 20,000 shares executed, even though there appeared to be more than the requisite number of shares for sale at the time he entered his order into the trading system.

This real-world occurrence captures the idea of phantom liquidity. While HFTs may trade against small orders, they tend to cancel their orders when a large order, like in this case, hits the market.

A second way through which HFTs may manipulate markets is smoking (also called layering). Again, this is easier to understand through an example.

In a stock, the current best bid price is 1,000 and the best ask price is 1,000.25. Let us say that the best ask price is posted by an HFT. However, no buyer in the market is willing to trade against the HFT’s sell order. The HFT submits sells orders at various prices like |1,000.05,|1,000.10, |1,000.15 and |1,000.20. These are at prices lower than the original sell order by the HFT, and hence improves the best ask price in the market. These orders appear long enough in the book to be publicly disseminated.

A trader sees these lower prices on the sell side and decides to trade against them by placing a buy order. By the time this buy order reaches the market, the HFT has already canceled the sell orders at |1,000.05,|1,000.10, |1,000.15 and |1,000.20. The buyer’s order ends up executing at the original best ask price of 1,000.25 and may be higher. By “smoking” the HFT briefly makes prices appear attractive to traders on the opposite side but withdraws those orders before their traders reach the market.

A third way through which HFTs may manipulate markets is spoofing. Here, the HFT manipulates the market from the side opposite to which she wants to trade.

Let us use the previous example. The best ask price of |1,000.25 is by an HFT. However, again, no one willing to buy from the HFT at this price. In order to “force” buyers to trade against her best ask price, the HFT places a large limit buy order at |999.90. Potential buyers infer that this large buy order is informed and prices are going to increase soon. They buy by trading against the HFT’s best ask price. The HFT cancels the large limit buy order once her order at the best ask executes. The HFT makes the other traders think that there may be information to force them to sell to her.

As the above HFT activities illustrate, they submit and cancel a large number of orders. Proprietary data from an Indian exchange from a few years ago show that about half of all orders submitted by algorithms and through direct market access accounts are canceled in India. Given the growth of HFT in India over the last few years, this number would most certainly be much higher today. 10% of these orders are canceled the same second as they are submitted, while another 14% are canceled within one second of submission. 62% of these canceled orders are in the publicly disseminated part of the order book, that is, the part of the market that all traders can see at all times. Given the possible actions of HFTs, these cancellations should not be treated trivially, especially the relatively larger orders.

In this day and age of automated trading and HFT, traders need to be careful while trading as they could fall prey to the manipulative practices of HFTs. While it is difficult for traders to beat HFTs on speed, exchanges offer various features and regulations that traders may use to protect themselves from HFTs.

– Authored by Prof. Ramabhadran S Thirumalai

References: Menkveld, A. J. (2016). The economics of high-frequency trading: Taking stock. Annual Review of Financial Economics,