Introduction

In today’s rapidly digitalising world, managing money has become as effortless as clicking a few buttons on a smartphone. Bill payments, money transfers, mutual fund investments, and even insurance purchases now happen instantly, without the need to step into a nearby bank. But with this convenience comes an important question: do we truly understand what we are doing with our money online?

Digital Frauds: A Growing Concern Worldwide

Consider the case of Dr Rahul Shukla (name changed), a 56-year-old senior consultant from Jaipur, India. One afternoon, he received a call that appeared to be from his bank, warning that his debit card could be blocked unless his KYC was re-verified. Worried, he clicked a link sent via SMS, which led to a website that appeared to be his bank’s. Trusting the interface, he entered his account number, Aadhaar details, card credentials, and OTP. Like many others, Dr Rahul Shukla became a victim of digital fraud, a growing menace in the age of online finance.

His experience is not unique, and this is not a single and isolated case. Digital fraud is a growing global concern. According to a UNODC report, digital fraud across East and Southeast Asia resulted in estimated financial losses of US$ 40 billion in early 2025, largely driven by organised crime groups in Southeast Asia. While these regions have been major hubs of cyber-enabled fraud, South Asian countries, including India, are also witnessing a rapid rise in digital financial fraud as digital payment systems expand and smartphone penetration accelerates. According to the Reserve Bank of India and NPCI, digital fraud complaints surged threefold alongside digital payments in FY 2025, reaching ₹30,014 crore, up from ₹12,230 crore the previous year. From fake UPI links and QR code scams to phishing and screen-sharing traps, fraudsters are becoming increasingly sophisticated, often exploiting users who lack awareness of safe digital practices.

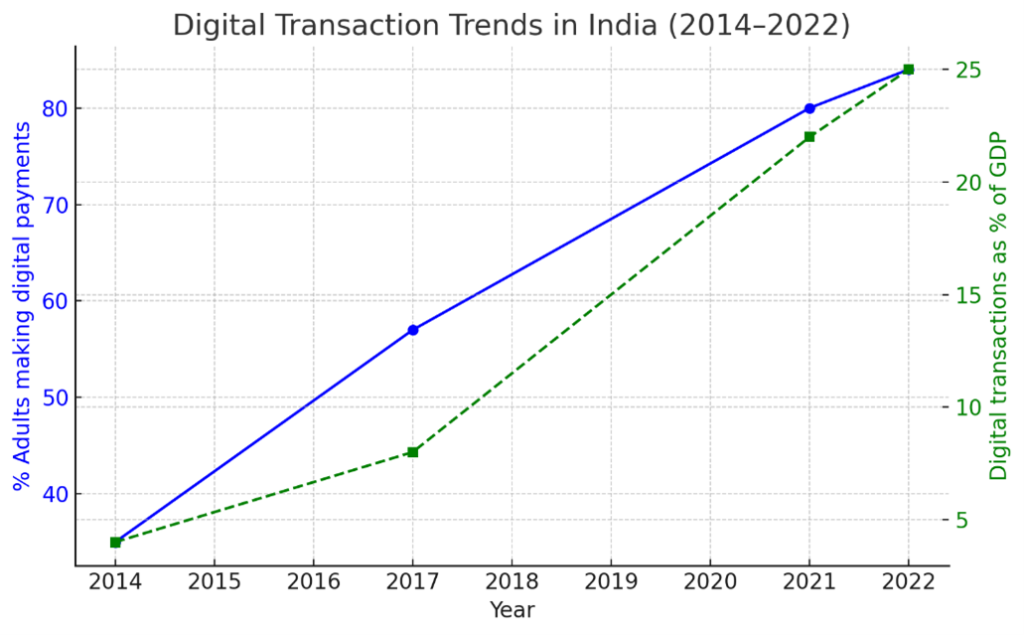

At the same time, India has witnessed a massive transformation in financial inclusion through digital technology-driven initiatives such as Jan Dhan Yojana, the Digital India program, and the Unified Payments Interface (UPI). Over the past decade, millions have embraced digital wallets, fintech apps, and online banking for their day-to-day money transactions. With a vision to transform India into a technology and digitally empowered society, the Government of India launched the “Digital India” initiative on July 1, 2015. This programme has played a central role in enhancing citizens’ access to public services through digital platforms, while simultaneously supporting the expansion of the digital economy and generating new employment opportunities. As a result of these efforts, India experienced a remarkable rise in internet penetration, with the number of users increasing by approximately 170 percent between 2018 to 2022 as per the World Bank Report. By 2022, approximately 80-85% of adults in India were making digital payments, reflecting a sharp rise in adoption of digital financial transactions (see Fig. 1). Looking ahead, this rapid digital adoption is projected to substantially expand the size of India’s digital economy, which is expected to grow from around US$ 50 billion in 2021 to nearly US$ 150 billion by 2025. This growth trajectory is being supported by policy-driven digital payments such as UPI, improvements in digital literacy, behaviorial changes following the COVID-19 pandemic, and the widespread availability of affordable mobile internet services. and the Digital India Initiative, rising digital literacy, pandemic-induced restrictions, and availability of cheaper mobile data, as reported by the World Bank.

According to the State of India’s Digital Economy (SIDE) Report, 2025, India ranks among the leading economies globally in terms of digital transformation, supported by its robust digital infrastructure. In line with the vision of achieving a “Viksit Bharat” (Developed India) by 2047, the Government of India has adopted inclusive development strategies focused on social welfare, education, and skill development. Through initiatives such as Digital India, these efforts seek to promote inclusive growth, foster innovation, and enhance India’s role in the global digital economy.

Despite these technological advancements, a segment of the population still lacks the knowledge to use digital platforms safely and effectively. This knowledge gap, too, has real consequences in financial decisions, including overborrowing, wrong investments, and falling prey to digital fraud. It is here that digital financial literacy becomes a critical life skill, a foundation not just for safe transactions but also for long-term financial well-being.

Fig 1. India’s digital transaction adoption trend (2014–2022)

Source: Author’s estimation based on RBI report on trends and progress of Banking in India

Financial Well-being through Digital Literacy

Digital financial literacy goes beyond operating smartphones or online platforms. It involves understanding systems like UPI, NEFT, and IMPS, performing secure digital transactions, recognising scams, and knowing one’s rights as a digital consumer. When individuals possess such knowledge, they can make informed financial decisions, manage money effectively, and avoid fraud. This contributes directly to financial well-being, which is not just about wealth but also about stability, confidence, and freedom to manage expenses, handle financial shocks, and achieve long-term goals while enjoying life’s pleasures without the stress or guilt of overspending.

Challenges in India’s Digital Financial Ecosystem

Despite impressive strides in financial inclusion, significant hurdles remain in India’s digital financial ecosystem. The rapid growth of digital payments, particularly through UPI, which recorded over 228 billion transactions in 2025 (NPCI), has brought millions of first-time users who are unaware of safe digital practices and fall victim to scams. Others assume they are digitally savvy but underestimate the creativity of fraudsters. As a result, 49 % of year-on-year (2025 ) increased cases of cyber fraud have been reported by the National Crime Records Bureau (NCRB), which indicates a steady increase in online financial fraud complaints in recent years. The digital divide continues to leave behind rural populations, older adults, and those with limited education. Meanwhile, the sheer complexity of financial products and fintech apps can overwhelm even regular users, leading to errors and poor decisions. Although regulators and banks introduce safeguards, criminals often exploit loopholes faster than these protections can be effectively strengthened. These challenges reveal why digital financial literacy must be treated not as optional knowledge but as a core life competency.

In Conclusion

Digital financial literacy is not merely about learning how to use apps; it involves gaining the knowledge and confidence to make secure, informed, and future-focused financial choices. As India marches toward the vision of “Viksit Bharat 2047,” strengthening digital financial literacy will be crucial to ensure that the rapid expansion of digital finance enhances citizens’ financial well-being rather than exposing them to severe financial fraud. The ability of its citizens to use digital tools responsibly will determine how inclusive and sustainable this growth becomes. From a policy perspective, collaborative efforts by regulators, financial institutions, and educational bodies are required to integrate digital financial education into academic curricula, public awareness programs, and initiatives that promote awareness and transform the technology into a tool for financial empowerment. Special attention should be given to vulnerable groups such as first-time digital users, rural populations, and the elderly. Strengthening digital financial literacy can empower individuals to make safer financial decisions, mitigate fraud risks, and ultimately enhance long-term financial well-being. Thus, from clicks to confidence, the journey begins with knowledge, and with it, financial well-being moves from aspiration to reality.

Anju Gupta is a Faculty Associate at T A Pai Management Institute, Manipal Academy of Higher Education, Manipal, India. Her research focuses on financial wellbeing and financial vulnerability, with particular interest in understanding how these factors shape healthy financial behaviour.

Deepak Kumar Behera is a Lecturer at The Business School, RMIT University Vietnam, Ho Chi Minh City, Vietnam. His research interests lie in health economics and development economics, with a focus on understanding socio-economic determinants of health outcomes and policy implications in developing country contexts.

Dil Bahadur Rahut is Vice Chair (Research) and Senior Research Economist at the Asian Development Bank Institute, Tokyo, Japan. His research focuses on development economics, agricultural economics, and climate change, with particular emphasis on sustainable development, rural livelihoods, and policy-oriented research in developing economies